Credit Tier Breakdown, Part 4: Bad Credit

A brief primer on credit score ranges

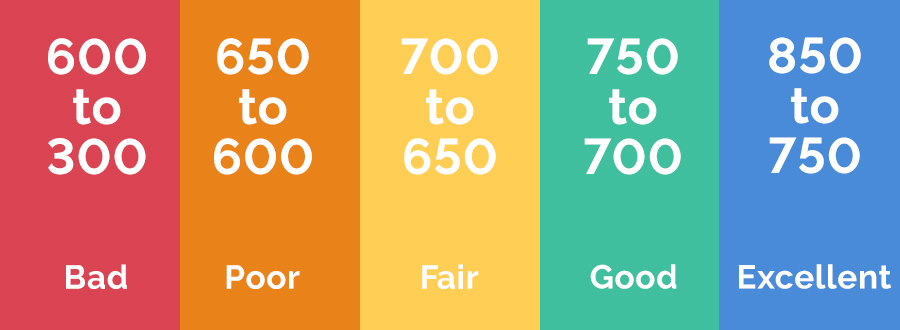

Credit scoring agencies have generally stuck with a system of Bad—Excellent,” say Ian Atkins, an analyst and staff writer for Fit Small Business.

“That scale can be useful,” says Atkins. "But lenders tend to use a different kind of shorthand that takes into account not only credit history but also other factors, like income and net worth.”

“Prime and super prime (or good and excellent) borrowers are those judged to have very low risk of default,” Atkins says. “That means low debt to income ratio, low debt to credit ratio, great payment history, long credit history, and good mix of credit types. These borrowers get better rates, better terms, better rewards and incentives, and lower fees on everything from credit cards to mortgages. In other words, it pays to be prime.”

On the other hand, having bad or poor credit—basically a score under 630—and landing in that subprime range doesn’t pay at all. In fact, it’s quite the opposite. Having a score in this range means that you will be the one paying more for personal loans—through higher interest rates and larger down payments.

What Kind of Loans Can You Get?

With a score under 630, loans from a traditional lender are pretty much off the table. Banks will deem you too big a risk to lend to at the rates that they are able to offer. You might have better luck with a credit union, but even then, you’re probably going to come up empty-handed.

You will likely not qualify for a mortgage either, although a score of 600 or above might qualify you for a subprime mortgage. These mortgages come with much higher rates than normal mortgages, and some of them come with rates that are “adjustable.” More on those later.

One type of traditional loan that you can qualify for even with a score below 600 is a subprime auto loan. The story here is much the same as the one for subprime mortgages. You will pay much higher interest rates, and you will likely be asked to put down a larger down payment in order to secure the loan.

When it comes to credit cards, you will see the number of offers you receive in the mail go down if your score drops into this range. And the offers you do receive will come with much lower credit limits, high-interest rates, and might even be for “secured” cards that require collateral.

Basically, if you have bad credit and need to borrow money, your options are going to be limited and your rates are going to be high. If you have a score under 600, pretty much the only loans you’re going to qualify for are “bad credit” and/or “no credit check” loans.

What are Bad Credit and No Credit Check Loans?

When it comes to bad credit and no credit check loans, you're going to want to be careful. While there are many legitimate lenders who lend to folks with bad credit, there are also lots of predatory lenders who are simply looking to take advantage of folks who don’t have many options.

Regardless, the principals for these loans could be smaller than traditional loans, and the interest rates could also be much higher.

The reason for this is simple: the lower a person’s credit score, the bigger risk they pose to a lender. A score below 630 indicates that you have a history of not making payments on time, taking on too much debt, and maybe even defaulting on loans entirely.

Bad credit lenders need to charge higher rates in order to guard against the higher rate at which their borrowers will default on their loans. If the lender didn’t do this, they would go out of business.

The two most common kinds of bad credit loans are payday loans and title loans. Both are short-term loans that come with average interest rates around 300%.(For all the ins and outs of bad credit loans, visit the TheLending Guide to Bad Credit Loans here.)

Payday loans are small-dollar loans that only average about 14 days, and they are often “secured” by a post-dated check that the borrower makes out the lender for the amount owed. On the due date, the lender deposits the check, and the loan is repaid.

The appeal of payday loans is that borrowers are able to pay the loans back quickly, but those short payment terms can also make a loan harder to repay. Since borrowers have to pay the loan back in full—instead of paying it back a little bit at a time like they would with an installment loan—the short turnaround can leave them without the necessary money.

In situations like this, the payday lender will then offer to roll the loan over, meaning that the borrower pays only the interest owed on the loan and then gets a new repayment term… complete with an additional interest payment. Rolling a loan over multiple times can drastically increase the cost of borrowing, all while leaving the borrower no closer to paying back the principal than they were when they first took it out!

With title loans, the borrower puts up their car, truck, or motorcycle as collateral. This allows someone to borrow a larger amount of money, but it also means that they will lose their vehicle if they can’t pay the loan back. The average term for a title loan is one month, and the average interest rate is 25%. With high rates and short terms, loan rollover can be a big problem for title loan customers as well.

There are also many lenders who offer installment loans to people with bad credit. These loans come with longer repayment terms than payday or title loans, usually somewhere between three and six months. Installment loans are paid off in a series of equal, regular installments, which can make paying the loan off a more manageable process.

The term “no credit check” loans describes loans in which the lender does not perform a credit check during the application process. A "hard credit check" can temporarily lower a person’s score, which makes no credit check loans appealing to folks who already have bad credit.

Some bad credit lenders do perform a "soft credit check" during the application process, which returns less information than a hard check, but does allow the lender to get a basic snapshot of the borrower’s ability to repay their loan.

In general, a lender who performs a "soft credit check" is likely preferable to one who performs no credit check at all. It shows that the lender is considering your ability to repay your loan the first time instead of hoping you roll it over again and again and again.

What kind of interest rates can you get?

According to the MyFico Loan Savings Calculator, a person with a 620 score who took out a $300,000, 30-year, fixed-rate mortgage would get an interest rate of 5.51% and would pay over $103,000 more in interest than a person with a score of 760.

However, some subprime mortgages have interest rates higher than that. In 2014, CNN Money reported that some subprime mortgages were being offered with rates from 8 to 10%. These mortgages also required a larger down payment, between 25 to 35% of the home’s total value.

The thing to really watch out for with subprime mortgages is rates that are “adjustable.” Oftentimes, these mortgages start with a low “teaser rate” that can make the mortgage seem much more affordable than it really is. When the teaser rate expires, these adjustable rates will shoot up, taking your monthly payments with them. This can lead many borrowers to default. (Adjustable rate mortgages were a huge factor in the financial crisis in 2008.)

The MyFico Loan Savings Calculator also estimates that a person with a credit score of 550 would pay an interest rate of 15.159% for a 30,000, 60-month auto loan. They would end up paying over $10,000 in interest more than a person with a score of 720 and an interest rate of 3.519%.

When it comes to unsecured personal loans, people with bad credit will generally be looking at an above-36% APR lender. This means that the annual interest rate that you pay on your loan will be above 36%, or 3% per month. While there are above 36%that will give you fair terms, reasonable rates, and good customer service, there will also be lenders in this space that are looking to take advantage of you—so be careful!

With payday and title loans, the interest rates you’ll get will vary from lender to lender and (more importantly) from State Financial Resource Guides state to state. But even though the rates will vary, they are still going to be incredibly high.

A 14-day payday loan with an interest rate of $15 per $100 borrowed would carry an APR of almost 400%! Meanwhile, a title loan with an interest rate of 25% per month would have an APR of 300%.

Payday loans are generally the most expensive and risky ways for people with bad credit to borrow money. Do your research when shopping for a bad credit and no credit check loan to make sure that the lender you’re working with is going to give you the best possible rates and most reasonable terms.

What can I do to raise my credit score?

“I'd like to be optimistic about purchasing power of a person with a score below 550,” says Roslyn Lash AFC®, Founder of Youth Smart Financial Education Services. But she adds that “their life in terms of credit will be poor.”

Here are four actions that Roslyn recommends people with poor scores can take to repair their credit:

- Prepare a Budget. This is the first step because it will tell you how much money you have left after reducing non-essentials. This extra money can be applied toward your bills.

- Pay all your bills on time. Make a schedule of when your bills are due and use e-bills and auto-pay to make sure that you pay the correct amount when it’s due.

- Eliminate debt! Check out the debt elimination plan outlined at PowerPay.org, and also look at strategies like the Debt Snowball and the Debt Avalanche. Whatever you decide to do, you need to make a plan, and then stick to it

- If you need assistance, seek financial coaching.

If you have additional questions about credit scores, personal finance, or getting a loan with bad credit, hop on over to our Resource Page and have a look around.

Ian Atkins (@FitSmallBiz) is an analyst and staff writer for Fit Small Business. He covers small business finance with a focus on traditional and alternative small business lending. Ian has over 9 years working in personal and small business finance.

Roslyn Lash, (@RosLash) is an Accredited Financial Counselor and the founder of Youth Smart Financial Education Services. She specializes in youth financial education, adult coaching and works virtually with adults helping them navigate through their personal finances i.e. budgeting, debt, and credit repair. Her advice has been featured in national publications such as USA Today, TIME, Huffington Post, NASDAQ, Los Angeles Times, and a host of other media outlets.